Menu

Choosing the right mortgage broker can make all the difference in securing the best deal for your home loan. Whether you’re a first-time homebuyer, looking to refinance, or simply exploring your mortgage options, a good mortgage broker can save you time, effort, and money. However, not all mortgage brokers are created equal. With so many options available in New Zealand, it’s crucial to choose one that fits your needs, offers excellent service, and has the expertise to navigate the complexities of the mortgage market.

In this blog post, we’ll walk you through five essential questions you should ask before choosing a mortgage broker to ensure that you’re making an informed decision. At Best Mortgage Brokers, we’re dedicated to helping Kiwis find the best mortgage solutions for their financial goals. By understanding the right questions to ask, you’ll feel confident in choosing a mortgage broker that can guide you through the home-buying process with ease.

When it comes to choosing a mortgage broker, experience matters. A broker with a strong understanding of the New Zealand property and finance markets will have the expertise to help you navigate the various loan products, interest rates, and lending criteria available.

Why It Matters:

The New Zealand mortgage landscape can be complex, with various lenders offering different types of loans, conditions, and rates. Additionally, the Reserve Bank of New Zealand (RBNZ) has specific regulations and lending restrictions that can influence your loan eligibility, especially when it comes to Loan-to-Value Ratio (LVR) and other criteria.

An experienced mortgage broker will be familiar with these nuances and be able to advise you on the best mortgage options based on your financial circumstances, property type, and goals. They should also have a strong track record of successfully securing mortgages for clients in your situation, whether you’re a first-time homebuyer, looking to refinance, or need a low-deposit loan.

What to Ask:

One of the main reasons people choose to work with a mortgage broker is their access to a variety of lenders. Unlike a bank or a single lender, brokers have access to multiple lending institutions, including big banks, credit unions, and non-bank lenders. This increases the chances of finding a mortgage that best suits your needs.

Why It Matters:

Different lenders have different loan products, interest rates, and lending criteria. If you only go directly to a bank, you might miss out on more competitive rates or suitable products from other lenders. A broker who works with a wide range of lenders can present you with multiple options, ensuring that you get the best deal possible.

Additionally, brokers may have access to exclusive deals, special rates, or products that aren’t available directly to the public. This can be particularly useful if you have specific circumstances, such as a low deposit or a less-than-perfect credit history, that may limit your options.

What to Ask:

Mortgage brokers typically earn a commission from lenders when they successfully secure a loan for you. However, it’s important to understand how a broker is compensated and whether there are any fees you’ll need to pay for their services.

Why It Matters:

A transparent mortgage broker will be upfront about their fee structure and how they get paid. Some brokers charge a fee to clients for their services, while others only get paid by the lender. Knowing this will help you assess the true cost of using a broker and ensure that their interests align with yours.

If a broker is paid by the lender, it’s important to understand whether they are incentivized to recommend certain lenders over others. A professional and ethical broker should always prioritize your needs and offer unbiased advice, regardless of the lender’s commission structure.

What to Ask:

The mortgage process can be stressful, especially for first-time homebuyers or those unfamiliar with the paperwork and documentation required. A good mortgage broker should offer more than just advice—they should provide ongoing support to ensure the process goes smoothly from start to finish.

Why It Matters:

The mortgage process involves a lot of paperwork, negotiations, and potential delays. A broker should act as a guide and advocate, helping you understand the requirements, answering your questions, and ensuring that all the paperwork is submitted correctly and on time. They should also be available to troubleshoot any issues that may arise during the approval or settlement process.

Additionally, some brokers offer post-settlement services, helping you monitor your mortgage over time and advising you on options for refinancing, repayment strategies, or accessing better deals in the future.

What to Ask:

Trust is crucial when choosing a mortgage broker. One way to ensure you’re working with a reputable and reliable professional is to ask for references or testimonials from previous clients. Positive reviews from other homeowners can provide insight into the broker’s service quality, professionalism, and success rate in securing mortgages.

Why It Matters:

Reading testimonials or hearing from clients who have worked with the broker in the past can help you gauge the level of satisfaction others have experienced. This can give you confidence that the broker is trustworthy, knowledgeable, and capable of handling your mortgage needs.

A reputable mortgage broker should be happy to share client testimonials or even provide you with direct references you can contact for further feedback. This can also help you understand what to expect during your own mortgage journey.

What to Ask:

Choosing the right mortgage broker is an essential step in securing the best mortgage for your home. By asking these five questions, you can ensure that the broker you choose has the expertise, resources, and commitment to helping you achieve your homeownership goals.

At Best Mortgage Brokers, we pride ourselves on offering expert advice, a wide range of mortgage options, and transparent, customer-focused service. Whether you’re buying your first home, refinancing, or looking for the best mortgage rates, we’re here to help you navigate the process with ease.

Ready to take the next step? Contact Best Mortgage Brokers today to find the perfect mortgage solution for you! Our team of experienced brokers is here to help you secure the best home loan deal for your needs and goals.

For New Zealand homeowners and homebuyers, navigating the world of mortgages can feel overwhelming, especially when it comes to industry-specific terms. One critical concept in the mortgage process is the Loan-to-Value (LTV) ratio. Knowing what LTV is, how it affects your mortgage application, and why it’s important can help you make better-informed decisions and increase your chances of securing a favorable loan.

At Best Mortgage Brokers, we are committed to helping New Zealanders understand the factors that can influence their mortgage options. Here’s a detailed look into LTV and its significance.

The Loan-to-Value ratio is a calculation used by lenders to assess the risk level of a mortgage loan. It’s the percentage that represents the ratio of the mortgage loan amount to the appraised value or purchase price of the property (whichever is lower). Essentially, it helps lenders understand how much equity you have in the property you’re looking to finance.

Formula for LTV Calculation:

LTV Ratio = (Loan Amount ÷ Property Value) x 100

![]()

For instance, if you’re buying a house worth NZ$500,000 and you have a 20% deposit (NZ$100,000), your loan amount would be NZ$400,000. Using the formula, your LTV ratio would be:

Example Values:

Calculation Steps:

Result:

LTV Ratio = 80%

The LTV ratio is crucial for both the lender and the borrower. Here’s why:

The amount you put down as a deposit has a direct effect on your LTV ratio. For example:

Lowering your LTV ratio can lead to better mortgage terms. Here are ways to reduce your LTV:

In New Zealand, if your LTV ratio is above 80%, you may be required to pay mortgage insurance. Mortgage insurance protects the lender in case you default on the loan. While it adds to your costs, it can allow you to buy a home with a smaller deposit, even as low as 10%.

While it’s possible to get approved with a high LTV ratio, aiming for an 80% or lower LTV can offer the best balance between affordability and flexibility. A lower LTV often means a more manageable monthly repayment amount, greater flexibility with lenders, and access to better rates.

Refinancing an existing mortgage is another situation where LTV plays a role. If you’re looking to refinance, having a lower LTV ratio (due to property appreciation or loan repayment over time) can make it easier to qualify for competitive refinancing rates.

A professional mortgage broker, like Best Mortgage Brokers, can help you understand and manage your LTV ratio by advising on ways to improve your deposit, providing options that accommodate higher LTVs, and working with lenders to get you the best possible rate. Mortgage brokers know the local New Zealand market, and they can help you navigate unique scenarios like low deposit loans, first-time buyer options, or refinancing.

LTV is a crucial factor in mortgage decisions and can influence your loan approval, interest rates, and even your overall financial stability. Understanding your LTV ratio, and finding ways to lower it if necessary, can set you up for long-term success and financial health.

If you’re ready to take the next step in your home-buying journey or need assistance with your LTV ratio, reach out to Best Mortgage Brokers. We’re here to help New Zealanders find the best possible mortgage solutions for their financial goals.

When considering a mortgage in New Zealand, one of the first decisions you’ll need to make is whether to choose a fixed or variable rate. Both options have their own advantages and potential drawbacks, and the right choice depends on your financial situation, goals, and risk tolerance. At Best Mortgage Brokers, we understand how important this decision is, so we’ve prepared this guide to help you navigate the differences and benefits of fixed vs. variable rate mortgages.

A fixed rate mortgage locks in a specific interest rate for a set period, typically ranging from one to five years in New Zealand. This rate remains unchanged throughout the term, providing predictable monthly payments.

Understanding Variable Rate Mortgages

Understanding Variable Rate MortgagesA variable rate mortgage, also known as a floating rate mortgage in New Zealand, has an interest rate that can change based on market conditions. Your lender will adjust the rate periodically, so your monthly payments could go up or down.

| Feature | Fixed Rate Mortgage | Variable Rate Mortgage |

|---|---|---|

| Interest Rate | Stays the same for the term | Fluctuates based on market conditions |

| Monthly Payments | Fixed amount | Can increase or decrease |

| Flexibility | Limited; high break fees | High; often no break fees |

| Risk Level | Low risk | Higher risk |

| Ideal For | Budget-conscious borrowers, those seeking stability | Those comfortable with risk, potential savings |

The right mortgage choice depends on your financial goals, lifestyle, and risk tolerance. Consider the following questions to guide your decision:

In New Zealand, many homeowners opt for a split mortgage, combining both fixed and variable rates. This option offers the best of both worlds: the stability of a fixed rate and the potential savings of a variable rate. By splitting your mortgage, you can enjoy partial protection against rate hikes while still benefiting if rates decrease.

The New Zealand mortgage market is influenced by factors such as the RBNZ’s official cash rate, inflation, and the broader economy. Recently, the RBNZ has increased interest rates to control inflation, which may make a fixed rate appealing to those looking for security against future hikes. However, if you believe rates may stabilise or fall, a variable rate could be a cost-saving option in the near future.

Choosing between a fixed and variable rate mortgage is one of the biggest decisions you’ll make when financing a home in New Zealand. Fixed rates offer stability and peace of mind, while variable rates can provide flexibility and potential savings. If you’re unsure which path is best for you, a split mortgage might offer a balanced solution.

At Best Mortgage Brokers, we’re here to help you make the right choice. With our expertise in New Zealand’s mortgage landscape, we can guide you through the options and find the perfect mortgage for your unique needs. Whether you’re a first-time buyer or a seasoned homeowner, our team is committed to helping you achieve your financial goals.

Purchasing a home is one of the most significant financial decisions you’ll make in your lifetime. Whether you’re a first-time homebuyer or refinancing your existing mortgage, securing a mortgage in New Zealand can be a complex and daunting process. While many are excited about the prospect of homeownership, mistakes in the mortgage application process can delay approval or, worse, lead to rejection. Understanding and avoiding these common pitfalls will help you streamline the process and ensure you get the best deal.

By being aware of these missteps, you can make informed decisions and increase your chances of a smooth and successful mortgage application process.

Your credit score is one of the most important factors that lenders use to determine your eligibility for a mortgage. It’s essentially a reflection of your financial health, showing how responsible you’ve been with managing credit and debt. The higher your credit score, the more favorable your mortgage terms will be, including lower interest rates.

However, many homebuyers in New Zealand fail to check their credit score before applying for a mortgage. This is a critical mistake because any issues with your credit report could negatively impact your ability to secure a loan. For example, outstanding debts, missed payments, or even errors on your credit report can lower your score and affect your mortgage approval chances.

Having a good credit score demonstrates to lenders that you’re a low-risk borrower, which means they’re more likely to approve your application and offer you better loan terms.

Many first-time buyers make the mistake of accepting the first mortgage offer they receive. However, mortgage rates can vary significantly across lenders, and even a small difference in interest rates can have a huge impact on your long-term payments.

New Zealand’s mortgage market offers a variety of options, from fixed-rate to floating-rate loans. Failing to shop around for the best rates could result in you paying more over the life of the loan.

Securing a mortgage with a competitive interest rate can save you thousands of dollars over the life of your loan. It’s worth investing time in comparing offers to ensure you get the most affordable option for your needs.

In New Zealand, most lenders require a deposit or equity as part of the mortgage application process. This deposit represents your share of the home’s value and is typically between 10% to 20% of the purchase price, although some lenders may accept as low as 5% for certain buyers (such as first-time homebuyers or those with a good credit history).

Many applicants make the mistake of underestimating the importance of having a solid deposit saved up. A small deposit could limit your mortgage options and lead to higher interest rates. On the other hand, a larger deposit will demonstrate your ability to manage money and may result in a lower loan-to-value ratio (LVR), improving your chances of mortgage approval.

A substantial deposit reduces the amount you need to borrow, which can improve your chances of securing a mortgage with favorable terms. It can also help you avoid costly LVR restrictions and Lender’s Mortgage Insurance (LMI) fees.

Your debt-to-income ratio (DTI) is a key factor that lenders use to assess your ability to manage additional debt. This ratio is calculated by dividing your total monthly debt payments by your gross monthly income. A high DTI ratio means that you’re already carrying a large amount of debt relative to your income, which can raise red flags for lenders.

Lenders in New Zealand typically prefer a DTI of 40% or lower when considering mortgage applications. If your DTI is too high, it can hinder your chances of getting approved for a mortgage, or result in you being offered a smaller loan amount.

Keeping your debt-to-income ratio low shows lenders that you have the financial capacity to handle additional debt and can make your mortgage repayments on time. This makes you a more attractive candidate for loan approval.

One of the most common mistakes is not being completely transparent about your financial situation when applying for a mortgage. Lenders rely on accurate and complete information to assess your application, and any discrepancies or hidden debts could result in delays, denials, or even legal consequences.

Honesty and transparency ensure that your mortgage application is processed efficiently. Lenders will appreciate your openness, which can lead to a quicker approval and more favorable loan terms.

The process of applying for a mortgage in New Zealand can seem overwhelming, but with the right preparation and knowledge, you can avoid the common mistakes that often lead to delays or rejection. By checking your credit score, shopping around for the best rates, understanding the importance of a solid deposit, keeping your debt-to-income ratio low, and being transparent with your lender, you’ll increase your chances of securing the right mortgage for your needs.

If you’re ready to begin the mortgage application process or need expert advice, Best Mortgage Brokers is here to help. We can guide you through each step, ensuring you avoid these common pitfalls and secure the best deal possible.

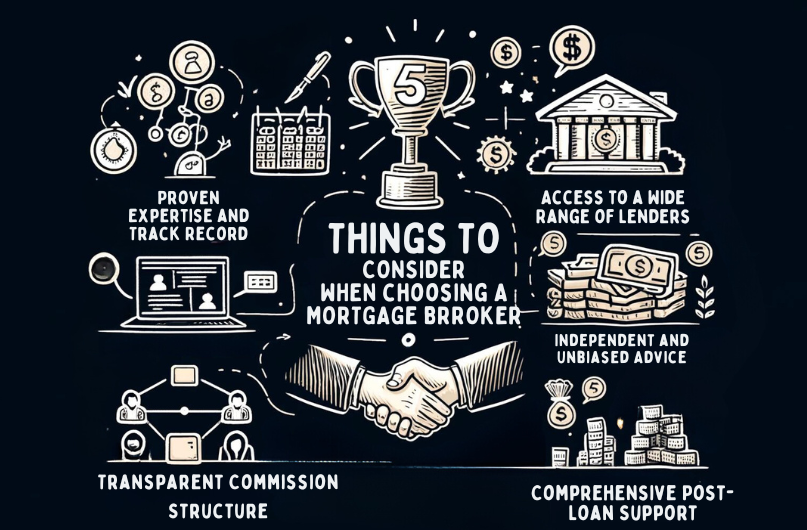

Buying a home is one of the biggest financial decisions you’ll make in your life. For most Kiwis, that means taking out a mortgage to finance their dream property. But with so many lending options and complex terms to navigate, the process can feel overwhelming. That’s where a skilled mortgage broker comes in.

A good mortgage broker acts as your guide and advocate, helping you secure the most favourable home loan for your unique situation. However, not all brokers are created equal. To ensure you partner with a professional who has your best interests at heart, there are several key things to look for.

In this article, we’ll walk you through the five most important factors to consider when choosing a mortgage broker in New Zealand. From their qualifications and lender networks to their independence and ongoing support, we’ll cover what you need to know to make a confident, informed decision.

By taking the time to carefully vet potential brokers using these criteria, you’ll be well on your way to securing a competitive mortgage that sets you up for long-term financial success. Let’s dive in and explore each of these critical considerations in more detail.

When choosing a mortgage broker, it’s crucial to assess their experience and qualifications to ensure they can guide you through the intricate process effectively. Understanding expertise begins with examining their track record. A broker with a history of successful mortgage applications is more likely to grasp the intricacies and requirements of different lenders, which can greatly boost your chances of approval.

When assessing credibility, consider the broker’s longevity in the industry. This isn’t just about the years; it’s about the depth of experience they’ve acquired and how they’ve adapted to changing regulations and market conditions. A seasoned broker can offer insights and solutions that less experienced brokers mightn’t even be aware of.

Furthermore, prioritize brokers who’ve consistently secured approvals. This indicates not only their proficiency in handling typical cases but also their ability in navigating complex scenarios. Opting for a broker with a strong approval history can provide you with a smoother, more predictable mortgage application process.

In essence, a mortgage broker’s qualifications and experience are crucial in achieving a tailored and successful mortgage solution. Make sure you’re entrusting your financial future to someone who’s proven their ability to handle it with expertise and integrity.

Drawing on the significance of a broker’s experience, their range of lender relationships is equally vital in securing a mortgage that best fits your needs. A broker with a wide array of lender options can offer customized solutions that align precisely with your financial situation. This variety guarantees that you aren’t restricted to generic products but have access to specialized mortgage plans that cater specifically to your unique circumstances.

Mortgage brokers with extensive broker connections are more skilled at maneuvering through the landscape of market rates. This ability to tap into a diverse network boosts their capability to secure competitive rates, ensuring you receive the most cost-effective mortgage options. Their established relationships with various lenders mean they can often negotiate better terms on your behalf, potentially saving you significant amounts of money over the life of your mortgage.

Furthermore, the flexibility offered by having access to multiple lenders proves invaluable, especially if you have specific requirements or face unique financial challenges. This diversity allows your broker to more effectively match you with a lender who not only meets but anticipates and accommodates your particular needs. Ultimately, the breadth and depth of a broker’s lender relationships can significantly influence the quality and suitability of your mortgage options.

Understanding the contrast between independent and affiliated mortgage brokers is crucial as it impacts the variety and impartiality of the mortgage options available to you. Independent brokers can provide you with unbiased advice because they aren’t tied to any specific lenders. This lack of conflict of interest means they’re free to explore a wider range of products, ensuring that the recommendations you receive are tailored to your unique financial needs.

On the other hand, affiliated brokers often face lender restrictions that can limit your options. These restrictions could mean that you’re not seeing a full spectrum of available mortgage products, potentially missing out on deals better suited to your situation.

Here are some key points to keep in mind:

Now that you know about the differences between independent and affiliated brokers, let’s explore how mortgage brokers get paid and the impact this has on your mortgage choices. Understanding the payment and commission structures is important for making informed decisions.

Mortgage brokers typically earn their income through commissions from banks, roughly amounting to 1% of the loan amount. For instance, on a $500,000 mortgage, a broker might receive a $5,000 commission. This similarity to travel agents’ earnings model means that you don’t directly pay fees to brokers; instead, their compensation comes from the lenders.

Commission transparency is vital. You should be aware of how your broker is compensated to ensure that the recommendations made are in your best interest rather than influenced by potential higher commissions from certain lenders. It’s also worth noting that some brokers might offer incentives like discounted interest rates or cash-back which can seem appealing but should be carefully evaluated against other loan features.

Understanding these payment options allows you to assess the full scope of what you’re being offered. Always inquire about how your broker is paid. This knowledge helps you gauge the impartiality of the advice you’re receiving, ensuring that your choice is truly the best for your financial situation.

After completing your mortgage, it’s important to select a broker who provides extensive post-loan assistance and services. This ongoing support is vital for effective financial planning and enhancing customer satisfaction. You’ll want a broker who isn’t just there at the beginning but stays with you, making sure that your mortgage management is as beneficial and streamlined as possible.

Choosing a mortgage broker who offers these post-loan services won’t only help you keep up with the dynamics of the housing market but also ensure you’re positioned well for any financial shifts. This level of support is vital in addressing post-loan challenges and opportunities, ultimately leading to a more controlled and satisfying mortgage management experience.

To choose your mortgage broker, verify their certification and local expertise first. You’ll want someone credible, with a proven track record and positive client feedback, ensuring they can tailor solutions to your needs.

To determine if a mortgage broker is good, check their credentials and seek out client testimonials. These indicators reflect their professionalism and effectiveness in securing favorable mortgage terms tailored to clients’ needs.

Don’t exaggerate your personal finances or use aggressive negotiation tactics with your mortgage broker. Misrepresentations can backfire, hindering your loan process. Always be straightforward to guarantee accurate advice and the best loan options.

When selecting a mortgage broker, make sure they have a solid track record and the right qualifications. A wide network of lenders can access better rates and options tailored to your needs. Choose an independent broker for impartial advice.

Understand their payment and commission structures to guarantee transparency. Don’t overlook the importance of thorough post-loan support.

By considering these factors, you’ll be well-equipped to find a broker who aligns with your financial goals and offers reliable guidance.

If you’re considering applying for a home loan it’s important to understand what the banks look for in the approval process. Banks assess your financial position and ability to service a mortgage and based on the level of risk you present, they determine how much they are willing to lend to you. In this update, we will explore the key measures used by banks to assess your risk and increase your chances of securing a home loan approval.

When it comes to assessing your income, banks not only consider the amount you earn but also your employment history, how long you have been in your current job, and if you are a PAYE earner or self employed. Banks also evaluate your employment status, whether you’re full-time, part-time, casual, or permanent, to gain a better understanding of your financial position. Self-employed applicants may face additional criteria due to higher perceived risk. To maximise your chances of a mortgage approval, you will need to have a stable income and demonstrate a consistent employment history. This will instil confidence in the banks that you have the financial stability to meet your mortgage repayment obligations.

Your credit history provides banks with valuable insights into how you manage your debts. A clean credit history increases your chances of a successful application as it demonstrates responsible borrowing behaviour. Before applying for a home loan, it’s advisable to obtain a copy of your credit file to check for any negative marks that could impact your application. The most popular sites to do this are Centrix Equifax or Illion. Maintaining a good credit score requires responsible financial habits, such as paying bills on time, keeping within your credit card limit and avoiding excessive borrowing. By diligently managing your credit, you can build trust with the banks and improve your eligibility for a home loan.

The size of your deposit plays an important role in determining your borrowing eligibility. A larger deposit reduces the risk for banks, making you a more attractive borrower. Saving diligently and accumulating a substantial deposit demonstrates discipline and financial responsibility. Regular and consistent deposits into your bank account showcase your ability to save, even while managing other expenses. By demonstrating your commitment to saving, you increase your chances of securing a successful home loan approval.

Good Account conduct is essential when applying for a home loan. The banks will look over your bank account statements to make sure you are managing your money responsibly. If you go into overdraft on your accounts regularly this can be seen as a negative so you will need to watch this closely. Having outstanding debts, such as credit cards or personal loans, can also impact your borrowing eligibility. Before applying for a home loan, it’s beneficial to try and pay off any existing debts. You could also consider consolidating multiple debts into one which can help to reduce your overall repayments, making you a more favourable candidate in the eyes of the banks.

Securing a home loan requires careful preparation and attention to detail. By understanding the key measures banks use to assess your risk, you can increase your chances of getting a home loan. Working with a Mortgage Adviser can provide invaluable guidance throughout the process, maximising your chances of success. With thorough preparation, you can navigate the home loan landscape with confidence and achieve your homeownership dreams.

Have you ever wondered why your bank might require you to lower your credit card limit and closing your buy now, pay later (BNPL) accounts like Afterpay and Laybuy? In this article, we delve into the reasons behind this recommendation and shed light on its impact on your financial journey, particularly when applying for a home loan.

Credit cards and BNPL schemes undoubtedly offer convenience and perks for everyday transactions, but it’s crucial to recognize that financial institutions view these as liabilities. This perspective can significantly influence the amount you’re eligible to borrow when seeking a home loan.

The dilemma arises for those who manage their credit cards and BNPL accounts responsibly – paying off balances monthly and avoiding interest charges. Despite these sound financial practices, banks still perceive the full credit card limit and active BNPL accounts as potential liabilities. This directly influences the serviceability assessment, a pivotal factor in mortgage approval.

While maintaining higher credit card limits and open BNPL accounts might provide a sense of security, it’s essential to realise that this can lead to unintended consequences when applying for a home loan. The seemingly unused credit cushion could actually hinder your borrowing capacity and result in unfavorable loan terms.

In many instances, lenders or your mortgage advisor will recommend either reducing your credit card limit or closing certain BNPL accounts. However, it’s essential to know that you’re not obligated to adhere to these suggestions. The decision to lower limits or close accounts should be aligned with your financial strategy and long-term goals.

Your credit card limit isn’t a fixed thing, and BNPL accounts can be managed based on your requirements. Once your home loan is secured, you can reconsider utilising these options as needed.

In conclusion, the relationship between credit limits, buy now pay later accounts, and mortgage applications is a complicated one. It’s essential to strike a balance between leveraging credit for convenience and ensuring that your financial decisions align with your home ownership aspirations.