Menu

Buying a home is one of the biggest financial decisions you’ll make in your life. For most Kiwis, that means taking out a mortgage to finance their dream property. But with so many lending options and complex terms to navigate, the process can feel overwhelming. That’s where a skilled mortgage broker comes in.

A good mortgage broker acts as your guide and advocate, helping you secure the most favourable home loan for your unique situation. However, not all brokers are created equal. To ensure you partner with a professional who has your best interests at heart, there are several key things to look for.

In this article, we’ll walk you through the five most important factors to consider when choosing a mortgage broker in New Zealand. From their qualifications and lender networks to their independence and ongoing support, we’ll cover what you need to know to make a confident, informed decision.

By taking the time to carefully vet potential brokers using these criteria, you’ll be well on your way to securing a competitive mortgage that sets you up for long-term financial success. Let’s dive in and explore each of these critical considerations in more detail.

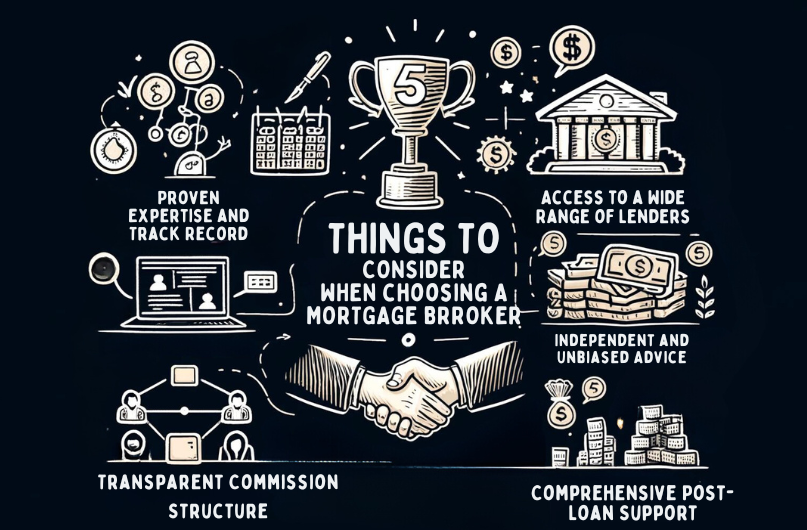

When choosing a mortgage broker, it’s crucial to assess their experience and qualifications to ensure they can guide you through the intricate process effectively. Understanding expertise begins with examining their track record. A broker with a history of successful mortgage applications is more likely to grasp the intricacies and requirements of different lenders, which can greatly boost your chances of approval.

When assessing credibility, consider the broker’s longevity in the industry. This isn’t just about the years; it’s about the depth of experience they’ve acquired and how they’ve adapted to changing regulations and market conditions. A seasoned broker can offer insights and solutions that less experienced brokers mightn’t even be aware of.

Furthermore, prioritize brokers who’ve consistently secured approvals. This indicates not only their proficiency in handling typical cases but also their ability in navigating complex scenarios. Opting for a broker with a strong approval history can provide you with a smoother, more predictable mortgage application process.

In essence, a mortgage broker’s qualifications and experience are crucial in achieving a tailored and successful mortgage solution. Make sure you’re entrusting your financial future to someone who’s proven their ability to handle it with expertise and integrity.

Drawing on the significance of a broker’s experience, their range of lender relationships is equally vital in securing a mortgage that best fits your needs. A broker with a wide array of lender options can offer customized solutions that align precisely with your financial situation. This variety guarantees that you aren’t restricted to generic products but have access to specialized mortgage plans that cater specifically to your unique circumstances.

Mortgage brokers with extensive broker connections are more skilled at maneuvering through the landscape of market rates. This ability to tap into a diverse network boosts their capability to secure competitive rates, ensuring you receive the most cost-effective mortgage options. Their established relationships with various lenders mean they can often negotiate better terms on your behalf, potentially saving you significant amounts of money over the life of your mortgage.

Furthermore, the flexibility offered by having access to multiple lenders proves invaluable, especially if you have specific requirements or face unique financial challenges. This diversity allows your broker to more effectively match you with a lender who not only meets but anticipates and accommodates your particular needs. Ultimately, the breadth and depth of a broker’s lender relationships can significantly influence the quality and suitability of your mortgage options.

Understanding the contrast between independent and affiliated mortgage brokers is crucial as it impacts the variety and impartiality of the mortgage options available to you. Independent brokers can provide you with unbiased advice because they aren’t tied to any specific lenders. This lack of conflict of interest means they’re free to explore a wider range of products, ensuring that the recommendations you receive are tailored to your unique financial needs.

On the other hand, affiliated brokers often face lender restrictions that can limit your options. These restrictions could mean that you’re not seeing a full spectrum of available mortgage products, potentially missing out on deals better suited to your situation.

Here are some key points to keep in mind:

Now that you know about the differences between independent and affiliated brokers, let’s explore how mortgage brokers get paid and the impact this has on your mortgage choices. Understanding the payment and commission structures is important for making informed decisions.

Mortgage brokers typically earn their income through commissions from banks, roughly amounting to 1% of the loan amount. For instance, on a $500,000 mortgage, a broker might receive a $5,000 commission. This similarity to travel agents’ earnings model means that you don’t directly pay fees to brokers; instead, their compensation comes from the lenders.

Commission transparency is vital. You should be aware of how your broker is compensated to ensure that the recommendations made are in your best interest rather than influenced by potential higher commissions from certain lenders. It’s also worth noting that some brokers might offer incentives like discounted interest rates or cash-back which can seem appealing but should be carefully evaluated against other loan features.

Understanding these payment options allows you to assess the full scope of what you’re being offered. Always inquire about how your broker is paid. This knowledge helps you gauge the impartiality of the advice you’re receiving, ensuring that your choice is truly the best for your financial situation.

After completing your mortgage, it’s important to select a broker who provides extensive post-loan assistance and services. This ongoing support is vital for effective financial planning and enhancing customer satisfaction. You’ll want a broker who isn’t just there at the beginning but stays with you, making sure that your mortgage management is as beneficial and streamlined as possible.

Choosing a mortgage broker who offers these post-loan services won’t only help you keep up with the dynamics of the housing market but also ensure you’re positioned well for any financial shifts. This level of support is vital in addressing post-loan challenges and opportunities, ultimately leading to a more controlled and satisfying mortgage management experience.

To choose your mortgage broker, verify their certification and local expertise first. You’ll want someone credible, with a proven track record and positive client feedback, ensuring they can tailor solutions to your needs.

To determine if a mortgage broker is good, check their credentials and seek out client testimonials. These indicators reflect their professionalism and effectiveness in securing favorable mortgage terms tailored to clients’ needs.

Don’t exaggerate your personal finances or use aggressive negotiation tactics with your mortgage broker. Misrepresentations can backfire, hindering your loan process. Always be straightforward to guarantee accurate advice and the best loan options.

When selecting a mortgage broker, make sure they have a solid track record and the right qualifications. A wide network of lenders can access better rates and options tailored to your needs. Choose an independent broker for impartial advice.

Understand their payment and commission structures to guarantee transparency. Don’t overlook the importance of thorough post-loan support.

By considering these factors, you’ll be well-equipped to find a broker who aligns with your financial goals and offers reliable guidance.

If you’re considering applying for a home loan it’s important to understand what the banks look for in the approval process. Banks assess your financial position and ability to service a mortgage and based on the level of risk you present, they determine how much they are willing to lend to you. In this update, we will explore the key measures used by banks to assess your risk and increase your chances of securing a home loan approval.

When it comes to assessing your income, banks not only consider the amount you earn but also your employment history, how long you have been in your current job, and if you are a PAYE earner or self employed. Banks also evaluate your employment status, whether you’re full-time, part-time, casual, or permanent, to gain a better understanding of your financial position. Self-employed applicants may face additional criteria due to higher perceived risk. To maximise your chances of a mortgage approval, you will need to have a stable income and demonstrate a consistent employment history. This will instil confidence in the banks that you have the financial stability to meet your mortgage repayment obligations.

Your credit history provides banks with valuable insights into how you manage your debts. A clean credit history increases your chances of a successful application as it demonstrates responsible borrowing behaviour. Before applying for a home loan, it’s advisable to obtain a copy of your credit file to check for any negative marks that could impact your application. The most popular sites to do this are Centrix Equifax or Illion. Maintaining a good credit score requires responsible financial habits, such as paying bills on time, keeping within your credit card limit and avoiding excessive borrowing. By diligently managing your credit, you can build trust with the banks and improve your eligibility for a home loan.

The size of your deposit plays an important role in determining your borrowing eligibility. A larger deposit reduces the risk for banks, making you a more attractive borrower. Saving diligently and accumulating a substantial deposit demonstrates discipline and financial responsibility. Regular and consistent deposits into your bank account showcase your ability to save, even while managing other expenses. By demonstrating your commitment to saving, you increase your chances of securing a successful home loan approval.

Good Account conduct is essential when applying for a home loan. The banks will look over your bank account statements to make sure you are managing your money responsibly. If you go into overdraft on your accounts regularly this can be seen as a negative so you will need to watch this closely. Having outstanding debts, such as credit cards or personal loans, can also impact your borrowing eligibility. Before applying for a home loan, it’s beneficial to try and pay off any existing debts. You could also consider consolidating multiple debts into one which can help to reduce your overall repayments, making you a more favourable candidate in the eyes of the banks.

Securing a home loan requires careful preparation and attention to detail. By understanding the key measures banks use to assess your risk, you can increase your chances of getting a home loan. Working with a Mortgage Adviser can provide invaluable guidance throughout the process, maximising your chances of success. With thorough preparation, you can navigate the home loan landscape with confidence and achieve your homeownership dreams.

Now is a great time to review your loan structure. Chances are, due to the high interest rate environment we are in, you will likely be coming off lower rates than what’s available now and for some time.

Regardless of whether you have a loan due to be refixed soon or not, it’s always worth reviewing to ensure that it’s set up to meet your current and future plans and goals.

It may have been some time since you last did this but plans, circumstances, jobs, income and life stages change so it is vital you review to make sure the structure suits you and minimises interest paid to allow you to become debt free quicker.

Economic and interest rate forecasts also change so this is another reason to review to ensure the structure takes this, and your interest rate strategies and risk appetite into account.

The review may be as simple as a quick health check to confirm its suitable or may be more in depth and involve restructuring, breaking and refixing, tweaking the repayments, interest only periods, increased borrowing for home improvements etc.

Even minor changes such as increasing repayments can have a big impact on how quickly you can become debt free and reduce your interest costs, though this may be a challenge in the current high interest rate environment.

There are other ways to reduce interest costs such as utilising a revolving credit facility. All banks have this type of facility, ANZ call it a Flexible Home Loan, ASB an Orbit, BNZ Rapid Repay and Westpac Revolving Credit etc.

The key benefit of revolving credit is that it can save you interest by reducing your daily loan balance as much as possible. Revolving credit loans are transactional accounts, like an overdraft in many ways. You have your salary paid directly into this account thus reducing the balance, as interest is calculated daily you keep the balance as low as you can for as long as you can. You can also make lump sum payments into the account and withdraw again when needed.

Another way is an offset loan, these work by linking your savings account to a loan and you only pay interest on the difference between the two balances. For example, you have $50,000 in savings and an offset loan with a balance of $100,000, the two accounts are linked so you only pay interest on the difference – $50,000. These types of account are great for those who need to keep funds separate (e.g. provisioning for tax & GST) but want to use those savings to reduce interest costs. Only Westpac, Kiwibank and BNZ currently offer these facilities.

These are just some of the options available to assist in paying the mortgage off quicker, I am here to help so please get in touch to discuss as you could shave years off your mortgage and save money!